REVISIONS TO SMALL BUSINESS DEDUCTION

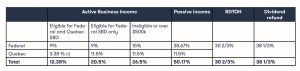

A summary of the tax rates applicable to CCPCs in 2021 and 2022 is set out in the following tables:

Combined Federal and Quebec corporate tax rates applicable on income earned in 2021:

[1] A tax rate of 3.2% is in effect in Quebec as of March 26, 2021. Before that date, the rate was 4%.This is due to an increase in the SBD reduction in Quebec to 8.3% from 7.5%. For a business with a December 31 year end, the rate for the year will be 3.38%.

Combined Federal and Quebec corporate tax rates applicable on income earned in 2022:

To understand the effect of these changes more fully and to plan for optimization, consider contacting your PSB BOISJOLI tax advisor.

Tax On Split Income

Significant changes have been made to income splitting strategies when dividends are paid by a company to its shareholders; these rules are known as the Tax On Split Income or TOSI rules. Starting in 2018, adult family members receiving dividends or other split-income, either directly from a private corporation or through a trust, will be subject to these rules. If the rules apply, the tax on split-income (equal to tax at the highest marginal income tax rate) will apply to split-income received by adult family members. The rules include several exemptions that can prevent amounts from being taxed at the top personal marginal tax rate.

The “excluded shares” exception exempts individuals who are 25 years of age or older and who own at least 10% of the votes and value of the company. The company must earn less than 90% of its income from providing services and cannot be a professional corporation and it cannot derive more than 10% of its income from another “related” business. A determination of whether the “excluded shares” exception applies is required each time an amount is received from the corporation.

If an individual is 65 years of age or older and his/her spouse is a shareholder of the individual’s company, the individual may be able to pay dividends to his/her spouse without TOSI applying. This is another exception to the rules.

In addition to the exceptions listed above, there are other exceptions based on the age group of the individuals receiving amounts from private companies, such as the “excluded business” exception, “reasonable return” exception, and “not from a related business” exception, to name a few. Given the complexity of the rules, a detailed review of the facts is necessary to determine the applicability of the exceptions.

Should you require additional information, please contact a member of our tax department.

Passive investment income

New tax rules were enacted for private companies earning passive investment income such as interest, capital gains and other non-business income. These new rules affect the ability for an operating company to benefit from the small business deduction on its active business income as well as limit when a company which pays a dividend could access its refundable dividend tax on hand. Should you require additional information, please contact a member of our tax department.

2021 YEAR-END PERSONAL TAX PLANNING CHECKLIST

OWNERSHIP OF FOREIGN PROPERTY

A revised Form T1135 was introduced by the Canada Revenue Agency to provide for more specific reporting on the ownership of foreign property. The form must be completed by any Taxpayer who owns foreign property with a total cost amount of more than $100,000 CDN at any time in the year. Such foreign property includes, but is not limited to, the following:

- bank accounts;

- shares of non-resident corporations (includes U.S.);

- debt owed to a Taxpayer by non-resident(s);

- interest(s) in foreign Trust(s);

- real estate; and

- other property except personal use property.

Where the total cost of all foreign property held at any time during the year was $250,000 or more, the form requires specific and detailed information such as identifying the name of each foreign entity in which funds are held or the name of each non-resident corporation in which shares are held.

This reporting must be done annually at the time of filing one’s personal income tax return. Failure to comply with these reporting requirements can attract a minimum penalty of $25 a day, for a minimum of 100$ and to a maximum of $2,500 per year and an incomplete filing can extend the normal reassessment period relating to that fiscal year.

If you are unsure about whether or not this impacts you, consider contacting us for a consultation.

FOREIGN AFFILIATE

Where a Canadian taxpayer owns a foreign affiliate (an equity percentage of 1% and an equity percentage of the taxpayer and each person related to the taxpayer of 10% in the foreign corporation) or a controlled foreign affiliate, the Canadian taxpayer is required to file a T1134.

Starting with the 2021 taxation year, there are several changes to this form.

The form will have to be filed within 10 months following the end of the taxation year for taxation years beginning in 2021 instead of 12 months for taxation years beginning in 2020 and 15 months for previous taxation years. In addition, several reporting requirements have been added, making it more difficult for taxpayers to ensure they have a complete and accurate T1134 form. It is important to mention that the Canada Revenue Agency has indicated that penalties will apply for forms with incomplete or inaccurate information.

For any clarifications, do not hesitate to contact your tax advisor at PSB BOISJOLI.

REGISTERED RETIREMENT SAVINGS PLAN

The deadline for 2021 RRSP contributions will be March 1st, 2022. Make your annual RRSP contributions early in the year to begin tax-free compounding as early as possible.

The amount deductible in 2021 is the balance of the unused contribution room as at December 31, 2020 plus the lesser of: 18% of 2020 “earned income” and $27,830, reduced by the 2020 Pension Adjustment.

Unused contribution room is the amount of RRSP deductions you are entitled to deduct from previous years less the amount actually deducted.

Consider asking your employer to make a direct contribution to your RRSP. The primary advantage of this type of contribution is that you can contribute your salary without your employer having to withhold federal and provincial income taxes.

The Canada Revenue Agency (CRA) allows taxpayers to over contribute to their RRSP up to a cumulative excess of $2,000. Making an over contribution may be advantageous because it will allow you to earn tax-deferred income even though you are not permitted to deduct the RRSP over contribution.

If you are over 71 years of age and you have earned income, consider making contributions to a spousal RRSP if your spouse has not yet reached the age of 71 in 2021.

If your 2021 taxable income is low and you anticipate earning more in the future, consider carrying forward your RRSP contribution and claiming a deduction in a future year to claim your deduction in a higher tax bracket.

If you receive a retiring allowance, consider transferring it directly to an RRSP (up to the deductible amount) to avoid withholding tax.

Any RRSP administration fees should be paid outside the plan; this will allow you to maximize the capital in the plan for future growth.

If you turn 71 during 2021, make your annual RRSP contributions before December 31st. Furthermore, your RRSP must be converted to either a Registered Retirement Income Fund or an annuity prior to the end of the year.

If you turn 71 in 2021, consider making your 2022 RRSP contribution in December 2021 before the RRSP is wound up. While you will be subject to an over contribution penalty for the period between the date of over contribution and January 1, 2022, you will benefit from an RRSP deduction in 2022. (This assumes that you have earned income in 2021, that you cannot contribute to a spousal RRSP, and that you can benefit from the deduction in 2022).

Earned income generally includes:

- income from employment;

- income from carrying on a business;

- taxable support (alimony) received in the year; and

- net rental income.

Less the total of:

- losses from carrying on a business;

- net rental losses; and

- deductible alimony payments

HOME BUYERS’ PLAN

The Home Buyers’ Plan allows a “first time home buyer” to withdraw up to $35,000 of RRSP funds on a tax-free basis to purchase a home. For a family, each spouse is entitled to withdraw up to $35,000 from their RRSP for a total of $70,000.

You are a “first-time home buyer” if you and your spouse have not owned and lived in a home as a principal place of residence at any time during the five calendar years up to and including the year in which the funds are withdrawn. For instance, if you withdrew funds from your RRSP on October 31, 2021, in order to be considered a “first-time home buyer” neither you nor your spouse may have owned a residence at any time after January 1st, 2017.

If you withdraw funds from your RRSP under the Home Buyers’ Plan, you must acquire a home by October 1st of the year following the year of withdrawal. In our example, the deadline would be October 1st, 2022.

Amounts withdrawn under this plan must be repaid to your RRSP over a period not exceeding 15 years. The repayment period commences no later than 60 days after the second calendar year following the year in which the withdrawal is made. In our example, the repayments must start on or before March 1st, 2024.

In the year of withdrawal, you may claim an RRSP deduction. In order to obtain a deduction, the contribution must remain in the RRSP for a period of not less than 90 days before the withdrawal if that contribution is part of the withdrawal.

Keep in mind that withdrawing funds under this plan will result in the taxpayer forgoing the income that would have been earned on those funds during the period of withdrawal and the related tax-free compounding of that income.

Easing of the HBP eligibility rules in the event of a breakdown of relationship in 2021 and beyond

These rules are intended to allow a separated spouse to acquire the other ex-spouse’s share or to acquire a new home.

Separated spouses can be considered first-time buyers again and use the HBP if they meet the following conditions:

- Living apart from their spouse or common-law partner for at least 90 days

- Living apart from their spouse or common-law partner at the time of the withdrawal and if they started living separately from this person in the year the withdrawal is made or during the 4 previous years.

However, two specific cases may prevent the application of these rules. First, the borrower’s new spouse cannot be an owner of the purchased home. Secondly, if the buyer has already used the HBP before, the amount must be fully refunded.

First-time Home Buyer Credit – Federal and Quebec

For Federal purposes, if you acquire your first home as a principal residence, you may be entitled to a non-refundable tax credit of 15% of $5,000.

In order to qualify, neither you nor your spouse should have owned nor lived in a home as a principal place of residence during the year of the purchase or the four preceding calendar years.

For Quebec purposes, the non-refundable tax credit is also equal to 15% of $5,000, for a maximum amount of $750.

LIFELONG LEARNING PLAN

Individuals, resident of Canada, may withdraw up to $10,000 per year from their RRSP, provided they are enrolled in full-time training in a qualifying educational program at a designed educational institution for at least three months during the year. The cumulative limit is set at $20,000 per person.

Generally, withdrawals under this plan are repayable in equal instalments over a 10-year period, with the first repayment due no later than 60 days after the fifth year following the first withdrawal.

Or

REGISTERED EDUCATION SAVINGS PLAN

Registered Education Savings Plans (“RESP”) can be used to achieve income splitting with children. There is no annual contribution limit to an RESP as of 2007 and later years, however the lifetime contribution is limited to $50,000 per child. While the taxpayer is not entitled to a deduction for a contribution made in the year, investment income earned in the plan accumulates tax-free, and will only be taxed when received by the student.

In addition to your contribution to the plan, the federal government provides a Canada Education Savings Grant (“CESG”). No matter the family income, this grant will be paid directly into the plan and is equal generally to 20% of the annual RESP contribution for each beneficiary under age 18, to a maximum of $500 per year or $1,000 if there are unused credits from the previous year. There is a lifetime limit of $7,200 for each child.

Depending on family income and in addition to the basic grant discussed above, the CESG rate will be increased on the first $500 of annual contributions to an RESP in respect of a beneficiary who is under 18 years of age:

- 20% if the child’s family has net income for the year of $49,020 or less;

- 10 % if the child’s family has net income for the year in excess of $49,020 but no more than $98,040.

Furthermore, since January 1st, 1998, each minor child accumulates grant contribution room of $2,500 per year. Therefore, RESP contributions will attract a Canada Education Savings Grant up to the amount of that cumulative room. In this respect, a family that has been unable to contribute to an RESP for one or more years will be able to “catch up” in later years.

If the RESP beneficiaries do not pursue higher education, then the income and the contributed capital may be withdrawn but the Canada Education Savings Grant must be repaid to the government. Withdrawals of principal may be made without tax consequences. The withdrawal of income will be subject to both regular tax and an additional 20% tax (12% if Qc, and 20% other Cases). Up to $50,000 of the income withdrawal will be eligible for transfer to your RRSP, to the extent that you have contribution room.

In order to be eligible for the Canada Education Savings Grant, a beneficiary must have a social insurance number.

In 2007, the Quebec government introduced a new refundable tax credit to support education savings. This refundable tax credit will be granted to a trust governed by an education savings plan for beneficiaries residents of Quebec that has attracted a Canada Education Savings Grant.

In general, the Quebec financial assistance for education savings provided by the tax credit will be equivalent to 10% of the first $2,500 of annual contributions to an RESP for children under age 18. Depending on family income, an increase of up to $50 per year may be added to the basic amount.

The maximum lifetime limit of the Quebec refundable tax credit is $3,600 per child.

TAX FREE SAVINGS ACCOUNT

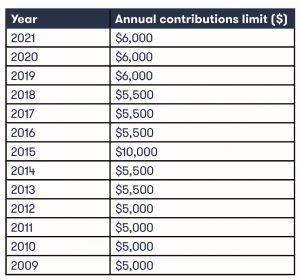

Tax Free Savings Account (“TFSA”): the TFSA was introduced in 2009. Unlike an RRSP, which provides for current tax deductibility on contributions and a deferral of tax on growth, the TFSA is not tax deductible for current contributions but is a tax-free vehicle thereafter. There will be no tax, including on withdrawal, of the funds or investments within the TFSA including the growth thereon. Individual resident Canadians were allowed to contribute $5,000 per year for the 2009-2012 taxation years so long as they were the age of majority. The contribution rate for 2013 to 2014 was set at $5,500 and $10,000 for 2015. It was returned to $5,500 for 2016 to 2018 and was established to $6,000 for the years 2019 to 2021. Any unused contribution room may be carried forward to future years. Therefore, as of 2021, a Canadian resident who was 18 in 2009 and has never contributed to a TFSA has a contribution limit of $75,500. Over-contributions are subject to penalties and interest.

Annual TFSA contributions limit

REGISTERED DISABILITY SAVINGS PLAN

A Registered Disability Savings Plan (“RDSP”) is a tax-deferred plan that was introduced as an incentive for parents and others to create long term savings for individuals who are eligible for the Disability Tax Credit. In brief, the RDSP works as follows:

- Only one RDSP can be created for a beneficiary,

- The disabled beneficiary must be a resident of Canada,

- Contributions into the plan are NOT tax deductible,

- Contributions will attract Canada Disability Savings Grants (“Grants”),

- Contributions may attract Canada Disability Savings Bonds (“Bonds”),

- Income accumulates in the RDSP on a tax-deferred basis,

- There is no maximum annual contribution limit,

- However, there is a maximum lifetime contribution limit of $200,000,

- Some planning is required in order to maximize a disabled beneficiary’s Grants and Bonds,

- Contributions can be made until the end of the year that the beneficiary turns 59.

CANADA DISABILITY SAVINGS GRANT

Grants are the amount that the Canadian government will pay into RDSPs. The amount of the Grant is dependent on the following two factors:

- a) the beneficiary’s family income, and

- b) the amount contributed into the beneficiary’s plan in the year,

The beneficiary’s family income is computed as follows:

- Until December 31ST of the year in which the beneficiary turns 18, the beneficiary’s family income isbased on the income information for the purpose of determining the Canada Child Tax Benefit for that beneficiary;

- Beginning in the year the beneficiary turns 19, the beneficiary’s family income is based on the disabled beneficiary’s income and that of his/her spouse,

- Where, in 2021, the beneficiary’s family income is equal to or less than $91,831, the Grant shall be computed as follows:

- o On the first $500 of contributions: 3 times the amount contributed (up to $1,500), and

- o On the next $1,000 of contributions: 2 times the amount contributed (up to $2,000),

As a result, the maximum annual Grant for low income families shall be $3,500 (on contributions of $1,500).

Where, in 2021, a beneficiary’s family income is more than $91,831 the Grant shall be computed as follows:

- On the first $1,000 of contributions: one dollar for each dollar contributed.

Thus, for high income earning families, the maximum annual Grant shall be $1,000 (on contributions of $1,000). Please note that the cumulative lifetime Grant limit is $70,000 per beneficiary.

CANADA DISABILITY SAVINGS BOND

In short, a Bond is another form of government assistance that is available for low income earning families. More precisely, the Canadian government will pay up to $1,000 per year to a RDSP where the beneficiary’s family income is equal to or less than $32,028. No Bond is paid where the beneficiary’s family income is in excess of $49,020. The amount of the Bond will be phased out where the family income is between $32,028 and $49,020. The cumulative lifetime Bond limit is $20,000.

Please note that no Grants or Bonds will be paid in years following the year the beneficiary turns 49 years of age.

TAXATION OF RDSP WITHDRAWLS

Generally, beneficiaries must begin to withdraw annual amounts from their RDSP in the year they turn 60 years old. The Grants, Bonds, and income generated within the RDSP will be taxed in the beneficiary’s hands as amounts are paid out of the plan. The original contributions, however, are not subject to taxation as they are withdrawn from the RDSP. Please note that the taxable portion is excluded from a beneficiary’s income when computing the GST/HST credit, Canada Child Tax Benefits, and the Working Income Tax Benefit. Further, it is excluded when calculating the social benefit repayment.

OTHER APPLICATION RULES:

Please note that all government Grants and Bonds paid into the RDSP during the ten preceding years must be repaid under any of the following circumstances:

- The RDSP is voluntarily terminated,

- The RDSP is deregistered,

- The beneficiary ceases to be disabled, or

- The beneficiary dies.

Please note that this article is not meant to replace a personal meeting to discuss this subject matter. Should you require additional information on RDSPs, please contact a member of our tax department.

DEDUCTIBLE EXPENSES / TAX CREDITS

To obtain a deduction or tax credit, the following items should be paid for before December 31, 2021.

- Registered pension plan contributions

- Investment counsel fees

- Union dues

- Professional membership fees

- Child care expenses

- Employment expenses

- Attendant care costs

- Tuition fees

- Moving expenses

- Medical expenses (*)

- Support (alimony) payments

- Charitable donations

- Interest expense

- Political contributions

- Acquisition of a first home that meets the requirements of the First time Home Buyer’s Tax Credit

- Physical education costs (fitness & sports) for children under 17 years old

- Interest on student loan

- Artistic, cultural, recreational costs for children under 17 years old.

(*) Disbursements in a period of 12 months ending in the year.

CAPITAL GAINS/LOSSES

Individuals can realize up to $892,218 (indexed for inflation in 2022 and subsequent taxation years) of capital gains free of personal income taxes when they dispose of Qualified Small Business Corporation Shares or Qualified Farm Property. Taxpayers holding such shares must ensure that the shares meet all eligibility criteria, or if not, steps must be taken to make the shares eligible.

The timing of when you decide to dispose of capital property is very important. For property that has appreciated in value, consider selling it only in January as opposed to the current calendar year. This can result in a one-year deferral of tax. Similarly, for property that had depreciated in value consider selling it before December 31, 2021. This will trigger a capital loss that can be used to offset any capital gains reported in the year.

In cases where you have realized large capital gains in calendar years 2018, 2019, or 2020 and you paid income tax on those gains at the top marginal tax rates, consider triggering capital losses to the extent of those gains prior to January 1, 2022. The purpose of the above is to allow you to recuperate taxes paid in prior years.

Note that any unused capital losses may be carried-forward indefinitely to be applied against future capital gains.

For investments in shares traded on the stock market, the selling date of the shares for tax purposes is the date of settlement of the transaction (i.e., two working days after the date of the transaction). For a sale of shares to be effective in 2021, the transaction must take place no later than December 29, 2021 for Canadian and U.S equities. Please contact us should you require further information regarding foreign or emerging market equities.

A capital loss incurred by an individual on the transfer of shares to his RRSP is deemed to be nil.

Gifts of publicly traded shares and stock options to registered charities may be eligible for an inclusion rate of 0 on any capital gain realized on such gifts. The result is that the otherwise taxable capital gain would not be included in taxable income.

SELF-EMPLOYMENT INCOME

Individuals residing in Quebec are required to pay contributions to the Health Services Fund (HSF) on non- salary income.

Self-employed individuals operating a successful business should consider whether incorporating the business would provide additional benefits. Many professional orders now allow their members to incorporate.

Self-employed individuals wishing to claim home office expenses must ensure that the work space is either:

a) the principal place of business of the individual; or

b) used exclusively to earn business income and to meet clients on a regular and continuous

Where the above-mentioned conditions are met, deductible expenses include, but are not limited to, a portion of property taxes, mortgage interest, rent, heat, electricity, insurance and other maintenance expenses. Where home office expenses create or increase a business loss, the amounts are not deductible against other sources of income, but they may be carried forward. This applies both federally and provincially.

HOME OFFICE (EMPLOYEES)

A large number of employees continue to execute their employment tasks by relying on teleworking due to the COVID-19 pandemic. Similarly to 2020, the ability to deduct home office expenses on their 2021 tax return remains an important issue.

You can deduct expenses paid during the year for the employment use of a work space in your home as long as you had to pay them under your employment contract. These expenses must be directly related to your work and must not have been reimbursed by your employer.

Also, one of the following conditions must be met:

- The home office is your main place of work (more than 50% of the time)

- This office is only used to earn your employment income and is used on a regular and continuous basis for meeting clients.

To confirm their responsibility for expenses under their employment contract, the employee must obtain from their employer a signed form T2200, Declaration of Conditions of Employment, which must be kept by the employee in the event of a CRA audit. For Quebec employees, a signed form TP-64.3-V, General Employment Conditions must also be obtained from the employer and submitted by the employee with their Quebec personal income tax return. The 50% threshold for performing the employee’s duties at home is generally calculated over the entire calendar year, or the relevant portion if employment began or ceased during the year.

For the general expenses that relate to the office and other part of the home such as the cost of electricity and heating, only a portion of them is deductible. The deductible portion of these expenses is calculated using a reasonable basis such as the area of the work space divided by the total area of your home. However, you cannot deduct property taxes, home insurance premiums, mortgage interest or claim the capital cost allowance on the building.

For the expenses related to the office only, you can fully deduct them. It could be a maintenance expense the cost of having your office walls painted for example.

Employees earning commissions

In addition, employees earning commission income can deduct, from that income, the portion of the property taxes and home insurance premiums related to the workspace. No federal deduction is available for Internet access expenses and cellphone or landline phone charges.

Internet fees can be deducted for Quebec income tax purposes only if they are billed according to use.

New simplified federal method

A simplified process was implemented for taxpayers who worked from home in 2020 due to COVID-19 and who had to cover modest expenses. CRA allowed to claim up to $400 based on the amount of number of days worked from home without the need to track detailed expenses.

To continue to support Canadians working from home due to the pandemic, the government will extend the simplified rules for deducting home office expenses and increase the temporary flat rate to $500 annually. These rules will apply to the 2021 and 2022 tax years.

Should you require additional information, please contact a member of our tax department.

CHILD CARE EXPENSES AND DISABILITY SUPPORT DEDUCTION

In the current context of the COVID-19, the Government of Canada has decided to temporarily relax the eligibility criteria for the child care expense deduction and the disability supports deduction for the 2020 and 2021 taxation years.

The Quebec government has chosen to harmonize with the federal government’s measures and has also relaxed its eligibility criteria for the refundable tax credit for child care expenses and the deduction for goods and services to support persons with disabilities.

These changes will allow recipients of Employment Insurance or Quebec Parental Insurance Plan benefits to benefit from these advantages for the 2020 and 2021 taxation years.

BUSINESS LOSSES

Some of the ways you may utilize losses realized in the year from an unincorporated business are:

- carrying the losses back three years and/or forward twenty years against other sources of income;

- collapsing RRSP’s;

- reducing or not claiming discretionary deductions; and

- accelerating receipt of other income (i.e. dividends).

PENSION INCOME

For taxpayers 65 and older, subject to certain threshold amounts, up to $2,000 for Federal and $2,939 for Quebec, of qualified pension income is eligible for federal and provincial tax credits. Qualifying pension income does not include Old Age Security or Quebec Pension Plan benefits.

If you are 65 or older and you are not in receipt of qualifying pension income, consider purchasing an annuity or converting your RRSP into a RRIF which will generate income eligible for the credit.

Since 2007, couples are given the option to split retirement income. This measure will enable taxpayers who receive retirement income, such as payments under a registered pension plan, annuity payments from a registered retirement savings plan (RRSP) starting at age 65 and annuity payments under a registered retirement income fund (RRIF) to allocate up to 50% of this income to their spouse.

INCOME SPLITTING

Spouses and children can be paid reasonable salaries from a family-run business. Note that the salary paid must be reasonable for the work performed.

Income attribution rules do not apply to capital gains earned on loans to minor children. Therefore, consider giving or loaning money to children to purchase investments with a low current yield but high capital gain potential. Although the income may be attributed to you, the capital gain will be taxed in your children’s hands and be subject to their tax rates.

Income splitting can be achieved in families with two working spouses by having the higher income earner pay as much of the family living expenses as possible and allowing the other spouse to save and invest his/her income. The overall purpose is to achieve taxation at the lowest possible marginal rate.

Income attribution rules do not apply to income earned on loans made to a relative (for example, a spouse, an adult child, or a trust created for the benefit of minor children) where the loan bears interest at the rate equal to (or greater than) CRA’s prescribed rates. The prescribed interest rate is 1% for the fourth quarter of 2021. Historically, the prescribed interest rate is comparably low. Although the interest on the loan would be taxable in your hands, the excess returns would be taxed at your relative’s tax rate. As mentioned above, the overall purpose is to achieve taxation at the lowest possible marginal rate. For additional application rules, contact a member of our tax department.

TAX INSTALMENTS

Ensure your required quarterly instalments are made on time to avoid non-deductible instalment interest and instalment penalty charges.

If your current year’s income is lower than the previous year, consider reducing your calculated instalments accordingly.

U.S. TAX ISSUES TO CONSIDER PRIOR TO DECEMBER 31

Have you spent more than 120 days in each of the last three years (including 2021) in the United States. If so, you should be filing Form 8840 “Closer Connection Exception Statement” to protect your status as a non- resident and to avoid having to file the FBAR “Report on Foreign Bank and Financial Accounts”. Note that the failure to file the FBAR on time, if required, results in an automatic $10,000 penalty.

Do you have any U.S. real estate and/or stocks and bonds? If so, you may be exposed to U.S. estate tax if the value of your worldwide estate is greater than 11 700 000 $US USD in 2021.

If you are unsure about whether or not this impacts you, consider contacting us for a consultation.

OTHER

If you are over the age of 65 and cash flow permits, consider delaying the application for your Quebec pension until the age of 70. Such a delay increases the pension amount by 0.7% for each month following your 65th birthday to a maximum of 42% at age 70.

If you are over the age of 65 and cash flow permits, consider delaying the application for your Old Age Security Pension until the age of 70. Such a delay increases the pension amount by 0.7% for each month following your 65th birthday to a maximum of 42% at age 70.

If you are considering making an acquisition that will allow you to claim CCA (capital cost allowance) (e.g. – automobile) consider making the purchase before the end of the year rather than early in the New Year. This will allow you to accelerate the CCA claim by one year.

Attempt to convert otherwise non-deductible interest expense into deductible interest. Using available cash pay down personal loans and credit card balances, and then borrow money for investment or business purposes.

Since interest rates on credit card balances are normally very high, consider refinancing alternatives such as a consumer loan or line of credit. This will significantly reduce the cost of non-deductible interest.

Consider Revenue Quebec’s rules that, since March 30, 2004, limit the deductibility of investment expenses for Quebec tax purposes to the investment income earned in the taxation year. Investment expenses that cannot be deducted in a given taxation year may be applied against investment income earned in one of the three preceding taxation years or in any subsequent taxation year.

Consider combining the claim for medical expenses. This will include eligible expenses incurred by you, your spouse, and your eligible dependents.

Since 2005, Revenue Quebec requires an employer that makes an automobile available to an employee to obtain from his employee a copy of the logbook that the employee keeps for the automobile, no later than the tenth day after the end of the year; or the tenth day after the end of the period in which the automobile was made available to the employee. If an employee does not provide his employer with the logbook within the prescribed time limit, he will incur a penalty of $200.